What Is The Affordable Care Act? Comprehensive Guide

Do you want to learn about the Affordable Care Act?

Do you want to know what you should look for before selecting a plan?

Well in this blog we have mentioned each and everything for your feasibility.

Learn new things in this blog and then apply for the plan that best suits your needs and budget.

The Affordable Care Act (ACA) known also as Obamacare has been a progressive and great law since the year 2010 when it was enacted. By bringing healthcare opportunities more and more to millions of Americans, ACA has brought a major change to the healthcare landscape.

Learning what this law is all about its various benefits as well as how to go through the system is vital, to ensure individuals and families can get competent healthcare services without spending too much.

Table of Contents

What is the Affordable Care Act?

The ACA, the popular name for the Patient Protection and Affordable Care Act, was introduced in 2010 and is considered one of the most important reforms in healthcare laws in a long while. Healthcare reform’s main goals include enhancing coverage levels, lowering costs, and improving the quality of treatment for the American people. The ACA covers a range of policies, including Medicaid expansion, health exchanges, and rules making health insurance companies stop discrimination on pre-conditions. By the law, every person has an insurance policy or must pay a penalty, with the offer of subsidies for low-income people to afford the coverage. In short, ACA has allowed thousands of people to have health insurance that is affordable and stay healthy. However, it still causes arguments between conservatives and liberals in the political world.

Establishment of the Affordable Care Act:

With President Barack Obama signing the ACA into law on March 23, 2010, after a drawn-out legislative session, the ACA became a success story of navigating through conflicts. These provisions were a culmination of the prior decades’ efforts to revamp the healthcare system and secure health insurance for millions of individuals. It is undeniable that since the enactment of ACA, this issue remains an important issue of debate in United States health policymaking.

Importance of the Affordable Care Act:

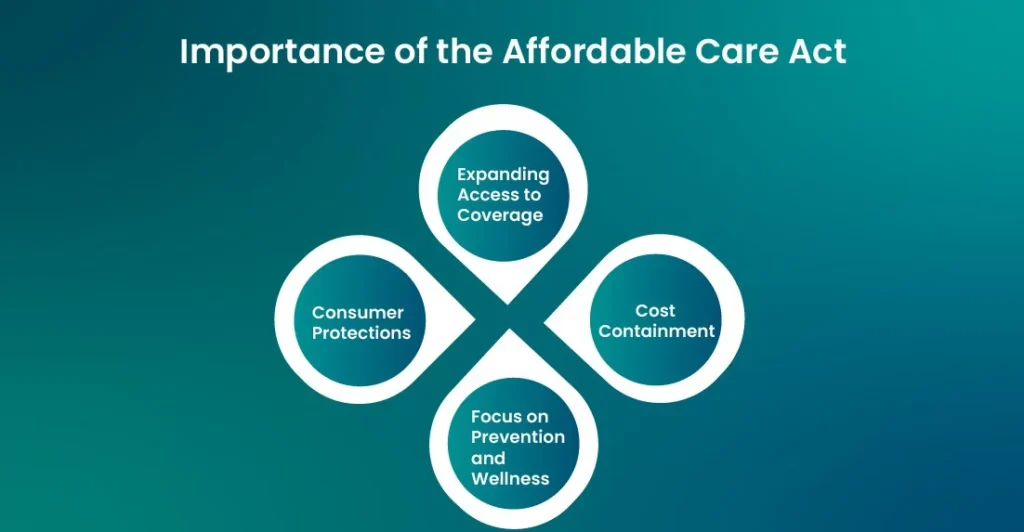

1. Expanding Access to Coverage:

A core objective of the ACA was to extend the inadequate amount of insurance for the population who had no health insurance or were underinsured. The ACA facilitated this access by expanding Medicaid, as well as setting up health insurance marketplaces; these prevented millions of mainly uninsured people from facing financial problems undergoing critical treatments.

2. Consumer Protections:

ACA inaugurated consumer protection provisions. These include among others: prohibiting insurance companies from not covering based on pre-existing conditions, capping the number allowed for emergency room visits and surgeries per year or the life of the insured, and higher premiums assessed based on health status. These provisions intend to facilitate all Americans to have partiality to full coverage and a sparing healthcare system.

3. Focus on Prevention and Wellness:

Interestingly, the ACA placed a strong emphasis on preventive care by requiring, in turn, insurance plans to cover all of the appropriate preventive services if the cost-sharing didn’t apply. ACA had the purpose of highlighting preventive measures such as screenings, vaccinations, and health assessments to promote better health outcomes and reduce future healthcare of consumers in the long term.

4. Cost Containment:

Apart from broadening the range of the care provided and upgrading the quality of care, ACA put in place a range of cost containment measures. By means such as value-based payment schemes, accountable care organizations, and attempts to lower unwarranted overuse, the ACA was an effort to improve healthcare delivery that would simultaneously be more efficient and effective.

Key Components Of The Affordable Care Act:

ACA was enacted into law by the then President, Barrack Obama, on March 23, 2010, with the overall aim of expanding health coverage, controlling healthcare costs, and improving the already existing quality of the healthcare sector. Key provisions of the ACA include:

1. Individual Mandate:

The ACA mandated most Americans to have health insurance to avoid paying a penalty. The motivation behind this rule was to expand the number of people who would be insured, which would help in diversifying the risk placed on insurers and ultimately reduce the cost.

2. Health Insurance Marketplaces:

The ACA created the platform of Health Insurance Marketplaces which serve as the mechanism for individuals as well as small-scale businesses to browse for and purchase appropriate insurance plans. The marketplaces sell various plans, sometimes with subsidies based on income to make health insurance cheaper.

3. Medicaid Expansion:

ACA has widened the Medicaid scope for people with income less than 138% of the Federal poverty line in their states and they would be qualified only if the expansion was adopted. It was to ensure that such ones who were not in a position to pay for the healthcare themselves were provided with insurance coverage.

4. Essential Health Benefits:

Each health insurance plan in the ACA has to cover a package of essential health benefits which are essentially preventive services, medically necessary care during pregnancy, prescription drugs, and mental health services. As a result, there are no gaps. All people have access to all health care plans.

5. Protections For Consumers:

The ACA has these consumer protections that are all included in it, for example, it prohibits insurance companies from denying coverage because of a person’s pre-existing conditions, it allows young adults to stay on their parent’s insurance up to the age of 26, and caps the amount a person has to pay out-of-pocket.

Pros and Cons Of The Affordable Care Act:

Pros:

- Expanded Coverage: Obamacare has been one of the trigger programs that led to a substantial reduction in the number of uninsured people, with hundreds of previously uninsured individuals gaining coverage.

- Consumer Protections: Individuals` security and tranquility were provided through the ACA by including new protections, for example, being covered for pre-existing conditions and no limit on the coverage amount.

- Focus on Prevention: The goal of ACA, by advancing preventive care and wellness efforts, was to generate positive health outcomes and, to some extent, the overall reduction of long-term health costs.

- Cost Containment Efforts: The ACA contained tools such as value-based payment models and delivery system reforms intended to cut costs. Those tools, along with a slowing rate of healthcare spending growth, contributed to the cost containment of the healthcare system.

Cons:

- Affordability Challenges: Although the authorities have made the coverage more affordable through the reduction of premiums, deductibles, and other costs, a major number of individuals are still finding themselves paying more than required, particularly those who aren’t eligible for the subsidies.

- Market Stability Concerns: Health insurance markets had fluctuations with risk-aversion insurers leaving some marketplaces and raising premiums due to ACA uncertainty and regulatory policy changes.

- Political Opposition and Uncertainty: The ACA has faced political resistance and legal challenges throughout its lifetime, leading to a volatile healthcare environment. The political side is manifested in ongoing uncertainties as new policies affecting healthcare in the country go in and out like fashion items.

- Medicaid Expansion Disparities: Not all states expanded Medicaid under ACA, the coverage disparities among low-income were growing, and the care accessibility disparities widened in non-expansion states.

Things You Should Look At Before Choosing A Plan:

1. Costs:

It is important to understand the total cost of treatment. Make sure you understand your premiums and out-of-pocket costs.

- A co-pay is a monthly bill you pay to your insurance company regardless of whether you use medical services. Fees may vary by plan

- Co-pays are the costs you pay to your health insurance company for the covered medical services you use. Deductible costs may include deductibles, deductibles, and coinsurance. For example, if you go to the doctor, you will likely pay a deductible that is for a specific service.

2. Cost Sharing:

See how your plan will share costs with you. ACA health insurance marketplace plans come in four “metal” categories: bronze, silver, gold, and platinum. Metal categories are based on how you and your plan share your healthcare costs. They have nothing to do with quality of care.

- Bronze plans offer the lowest monthly payments, but have the highest costs if you need care

- Platinum plans have the highest monthly payments, but the lowest outside-out-of-pocket costs if you need care

- Most people choose plans based on your family’s overall health and special care needs. Before you buy a plan, you can see an individual price estimate at HealthCare.gov/see-plans.

3. Network:

Make sure you look at the plan’s network of doctors/services. A network is a health plan that contracts with doctors, hospitals, pharmacies, and other healthcare providers to provide discounted services to plan members. Some plan types allow you to use any doctor or healthcare provider, while other plans limit your choices or charge you more if the providers you use are outside the plan’s network.

Who Qualifies For ACA Subsidies?

If you are confused with ACA, don’t worry! Discover our guide to the target criteria and submission procedure to apply for the medical coverage plan at an affordable price.

Eligibility criteria for ACA subsidies mainly operate on the grounds of family size and household income.

Here are the basic criteria:

- Income Range: Based on the FPL (Federal poverty level) your household income should be at the (100-400%) FPL percentage rate. On the other hand, states that have enabled citizens to qualify for Medicaid coverage may also have subsidies extended to households that have incomes below 100% FPL.

- No Access to Other Affordable Coverage: You are ineligible to receive public coverage, regardless of whether it is in the form of Medicaid, Medicare, or CHIP. Apart from that, you are not allowed to collect wages from an employment-related plan.

- Must File Taxes: You must file the federal income tax return for the year in which you are requesting the assistance unless the assistance is food stamps or a doctor’s appointment subsidy.

- Legal Residency: You should be either a United States citizen, a U.S. national, or lawfully present in the U.S. as the criteria to participate in the election.

- Purchase Through the Marketplace: Eligible individuals can get the subsidy by enrolling through the Health Insurance Marketplace.

How To Apply For ACA Subsidies?

Visit the Health Insurance Marketplace: Please go to the Health Insurance Marketplace’s main website (HealthCare.gov). If your state managed its marketplace through a state platform you would get there as well.

- Create an Account: If you’re new to the platform, you’ll have to create an account but thereafter your experience will be focused on retaining your customers. And if you’re returning, take the shortest path to the dashboard: either open the app or visit the homepage.

- Fill Out the Application: Upon submission of an application form, in which you will specify the particulars of your household, and income status as well as the available coverage options, you will commence receiving quotes from the insurance providers.

- Review Eligibility Results: Nonetheless, you’ll find out about the status of the application after you send the document and you are going to be advised in an eligibility determination notice. It will show you if you are eligible for ObamaCare premium assistance and its amount.

- Choose a Health Plan: In the case you are entitled to the subsidy, you can select the plan among such choices as health plans. The subsidy specified is the one that will be used to alleviate your monthly premiums.

- Stay Updated: Make certain that you state that the marketplace should be updated with major life alterations such as income adjustments or family growth size as they can dictate your subsidy eligibility.

Navigating The Affordable Care Act:

Navigating the ACA and accessing affordable healthcare involves several steps:

- Determine Eligibility: Visit your state’s social services website to see if you are eligible for Medicaid expansion by following the provided income guidelines. If enrolled in Medicaid, there could be the possibility of getting subsidies to buy coverage through the Health Insurance Marketplace if not eligible for Medicaid.

- Explore Coverage Options: Go to the Health Insurance Marketplace website or console a navigator/certified application counselor to help you analyze the various plans and choose the one that not only best suits your needs, but also your budget.

- Enroll During Open Enrollment Period: The ACA has an annual enrollment period annually which the consumers can enlist for a plan for the first time or make changes to their current plan on selected months During these six-month enrollment periods, consumers have two opportunities, in the fall and spring, to sign up for a Marketplace plan. Outside of this timeframe, enrollment is only possible if there is another coverage loss or a qualifying life event occurs.

- Understand Financial Assistance: The premium amount you pay is dependent on the income level, and you may qualify to receive a subsidy if your income qualifies for premium tax credits and cost-sharing reductions to cover your monthly premium and out-of-pocket expenses. The subsidies, which are provided to those who qualify for the Health Insurance Marketplace, may help people financially as they purchase the insurance.

- Stay Informed: Be informed of new regulations regarding the ACA that could include changes to health coverage options, subsidies, or enrollments. Make use of resources such as Healthcare.gov, health associations/organizations near you, and community outreach campaigns for information and support.

What If I Already Have Health Insurance?

If you or your spouse has employer-based insurance, the only way to get financial assistance from the New York State Health Plan is if your insurance does not meet the minimum affordability requirements. A work-based health plan is not considered affordable if premiums are more than 8.39 percent of the family’s household income.

If you are covered by private health insurance and not through your job, you can save significantly by switching to the New York National Health Plan. You can do this during Open Enrollment.

If you already have a New York State health plan but want to change your coverage, you can do so during Open Enrollment.

If you received a temporary extension of COBRA coverage and that coverage has ended, you may be able to enroll in New York State during the health plan’s 60-day special enrollment period. Try to apply and choose your plan before COBRA coverage ends to make sure there are no gaps in coverage.

Conclusion:

The Affordable Care Act has benefited millions of Americans in terms of health care accessibility which is now affordable due to the bills that have been put through. These bills not only protect but also provide crucial benefits. To appreciate ACA it is necessary to grasp its features, and channels through insurance plans and determine what it means for financial aid. The need to utilize the available resources as well as the support systems will enable people and families to be covered by healthcare coverage whose quality matches their requirements as well as the budget.

FREQUENTLY ASKED QUESTIONS:

Q: How can I find assistance with plan enrollment in my local area?

You can search for local help here. Just enter your zip code to find application assisters near you.

Q: Do I have to pay deductibles and copayments for essential health benefits?

Generally, yes. All ACA Marketplace plans have deductibles, copayments, and other out-of-pocket costs that apply to most covered services. Some preventive services are free, and some plans cover other services without out-of-pocket costs.

Q: What if I can’t afford coverage?

The Illinois Department of Insurance encourages you to get health insurance.

If you think you can’t afford coverage, there is help available. First, check out HeatlhCare.gov and see if you qualify for cost assistance or Medicaid based on your projected Modified Adjusted Gross Income (MAGI).

You can use the Kaiser Family Foundation’s coverage calculator to figure out if you qualify for assistance and how much your monthly premium will cost before and after assistance

Q: What is an ACA penalty notice?

Each year, ALEs must file Form 1095-C and Form 1094-C with the IRS, proving that they complied with the ACA. If either of these forms contains inaccurate information or misses the submission deadline, the employer may receive a penalty notice. In addition, ESRP notices are issued when timely, affordable, and appropriate benefits are not offered to full-time employees and their dependents. These notifications include the employees who triggered the ESRP, the incurred penalty – IRS Code Section 4980H(a), (b), or both – and the assessed dollar amounts for each violation.