How Does ACA Health Insurance Cost Influence & The Benefits Of Understanding This?

Do you want to under the ACA health insurance cost?

Well, this is the right place. In this blog, we have discussed everything in detail to make it easier for you to understand the terms related to ACA Health insurance costs.

Read this article thoroughly and select the right insurance according to your needs and financial stability.

Using the healthcare system in the United States calls for a great deal of skills when you are paying for your medical insurance and other treatments. Luckily, the ACA, or Affordable Care Act was put in place to assist the insurance industry in giving more people less expensive means of affordable health insurance. Nevertheless, we should ensure that we are aware of the specific costs that the health insurance within the ACA comes with before we enroll in a plan. Such things as monthly premiums, deductibles, co-payments, and the limit of out-of-pocket expenses are not just the only factors we include here. When people take time to read and compare different plans one after another they can understand good and bad ones the most and also come up with a better plan as they take advice from others.

In this blog, we’ll delve into the various factors that influence ACA health insurance costs and provide insights to help you navigate this complex landscape.

Table of Contents

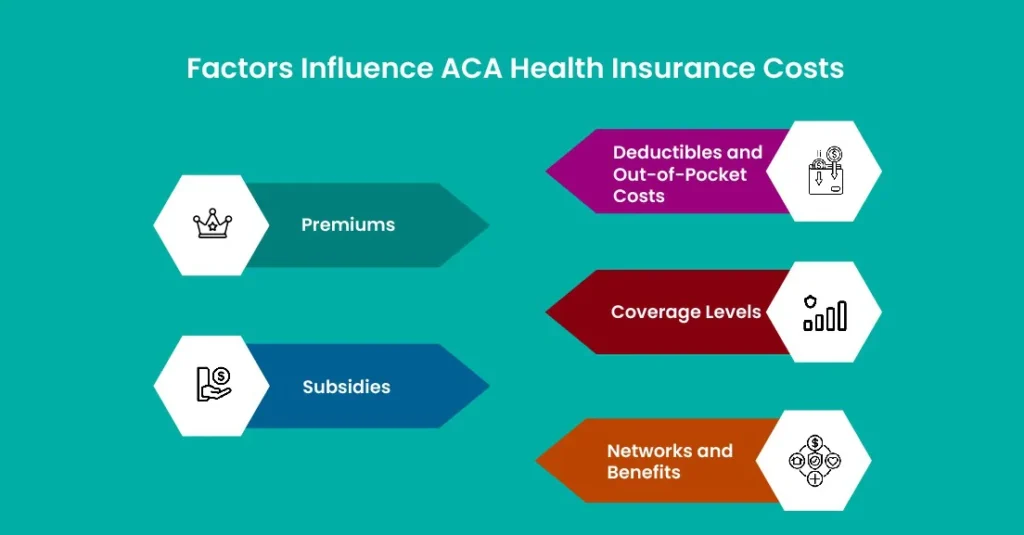

Factors That Influence ACA Health Insurance Costs:

1. Premiums:

The financial amount you pay every month for the coverage of health insurance is called a premium. The healthcare insurance plans with the ACA can be accessed via the Health Insurance Marketplace where you can compare the different available plans, among others, with their premiums, co-payments, and deductibles. Premium amounts may differ according to things like tobacco use, whether you’re living in urban districts or remote areas, differing levels of coverage, and choice in bronze, silver, gold, or platinum.

2. Subsidies:

Of the many elements of the ACA, one can point to the fact that there are subsidies provided to lower-income families and people who cannot afford any health insurance. The Premium Tax Credit (PTC) is a tax reduction that inputs money to your subsidized premium every month. These sums differ depending on the SRP you have and how many family members you are responsible for. Subsidy eligibility depends on the household income compared to the federal level, which is the amount used to determine eligibility.

3. Deductibles and Out-of-Pocket Costs:

Furthermore, medical services provided under ACA insurance plans are met with premiums and deductibles you have to pay so you have to contribute to these costs. The deductible refers to the portion of the amount you are expected to pay out of your pocket before start covering it. Inside pocket costs are comprised of the deductible that you pay, any copay you receive, coinsurance and any expenses not covered by your plan. The least expensive plans usually come with higher deductibles and at the same time, the ones with lower deductibles are mostly the more expensive ones.

4. Coverage Levels:

ACA health plans are placed in the four tiers of the metal structure (bronze, silver, gold, and platinum). The premiums of bronze plans are lowest, while the costs of their OOP share are highest, and conversely, for platinum plans the highest premiums are linked with the lowest personal CMS. Because the silver program is most common a person can get an extra part of premiums and a lower price of direct payment. The appropriate coverage amount is determined by the level of healthcare corroboration you are seeking along with the financial affordability.

5. Networks and Benefits:

Along with ACA health insurance options, it makes much sense to look for providers and advantages beforehand because they all might be different. When going with providers that are part of your in-network, you have already negotiated the rate with the insurance company which lowers your cost. Only in-network providers may have similar fees or may not be covered by your insurance policy at all. Furthermore, be aware of the types of procedures that are covered, particularly items like prescription drugs, preventive care, and maternity services.

The Open Enrollment Period is the period during which you can enroll for or re-enroll in an ACA-qualifying health plan. Alternatively, signing up for or changing plans would be possible for you outside of this period unless you have qualified life events, such as marriage, childbirth, and loss of other insurance coverage. Make sure you find your exact date on your calendar and avail the Open Enrollment Period to inspect the alternatives and change to the coverage that is positive for you.

Insurance costs under ACA can also be a complex issue, especially taking into account premiums, subsidies, deductibles, coverage levels, networks, and benefits, but you can still explore plans that fit you both medically and budget-wise. Be explored by possible choices in the Health Insurance Marketplace while the certified enrollment assisters could be contacted or insurance agents if the need is present. Through ACA being aware of the consequences of health insurance; one can make the right choice to protect both your health and financial security.

The Advantages of Understanding ACA Health Insurance Costs:

Health insurance and ACA may seem difficult and obscure. In the arena of healthcare costs, it is even worse. While this may be overwhelming it can also play a crucial role in enabling individuals and families to plan their budget for health insurance expenses. Having a clear picture of what costs are involved and the choices available, consumers have a chance to make an informed comparison about healthcare coverage and better manage their healthcare expenses.

Learning about the prices of ACA health insurance plans allows you to be confident that you have the necessary information which will help you think it through and select what is best fit for your specific healthcare needs and even have the time to review it by yourself.

1. Informed Decision-Making:

- It is an added advantage when ACA health insurance costs are evident to eligible individuals. They will also find it easy to select the best choice of plan that fits them perfectly.

- Therefore, this step of understanding how premiums, copayments, and out-of-pocket expenses are linked to their chosen plan helps them select the most appropriate plan according to their budget and healthcare scheduling.

2. Financial Planning:

- Getting aware of ACA health insurance rates as well as medical bills cost is a key thing that assists people people to not having problems budgeting for and providing for their medical expenses.

- As the year begins, the individual will be better off clarifying upfront about deductibles, plans, and what it could mean in the end in terms of the expense when seeking treatment. In this way, planning for healthcare finance will be easier and more timely.

3. Maximizing Value:

- ACA health insurance cost needs to enable this knowledge to maximize their health insurance value.

- When they compare various plans and assess where the sweet spot between premiums and benefits is they are better placed to select a plan that fits their health dollar needs.

4. Access To Subsidies:

- Knowing the premium tax credit and other subsidy criteria can allow people to calculate the costs of ACA and find out whether or not they qualify for that help.

- As part of the initial process, individuals may learn about subsidy eligibility criteria and income thresholds which work towards the reduction of the monthly premium cost for them.

5. Managing Healthcare Expenses:

- The comprehension of the ACA health insurance rates avails people in the proper management of healthcare expenditures.

- By grasping the concepts of deductibles, copayments, and coinsurance, individuals can determine their expenses budget and have the least dig into their pockets when seeking healthcare provision services.

6. Protecting Financial Well-being:

- Knowing how to work with the ACA health insurance cost is very vital for the safety of financial well-being of people and families.

- One of the most important tasks that one should take their time on when getting healthcare insurance is to choose a plan that offers adequate coverage at a price they can afford. By doing so, people won’t have to spend a lot of their income on medical bills or pay consultation fees whenever they get sick.

7. Ensuring Adequate Coverage:

- ACA health insurance cost is a knowledge paramount to any person because it is the most important factor to ascertain that you have sufficient coverage for your healthcare needs.

- By assessing coverage level, benefits, and providers along with the patient personal preference and health needs, the patient can make an informed and appropriate choice.

Conclusion – ACA Health Insurance Cost:

The Affordable Care Act (ACA) health insurance’s impact on the healthcare industry is several and comes with a relatively large number of positive changes. Among the many advantages of marketization is the fact that it has made people grasp the financial value of having insurance against health problems. This knowledge has led some people to take control of their decisions, which has helped them plan their finances in a better way, and maximize the amount of coverage accorded to them.

Finally, people are much more aware of all the cost factors, including premiums, deductibles, in- and out-of-pocket expenses, and other expenses that are essential for healthcare through ACA. This awareness has empowered them to assert themselves when dealing with the healthcare system and the payoffs of medical treatments. At present, those who are unhealthy are more likely to know the reason for their medical bills and make the right decisions to keep their financial health.

In conclusion, the ability to estimate and comprehend the ACA health insurance expenses compliance is an essential aspect of making informed choices for one’s health and financial well-being. The knowledge gained from understanding the costs and expenses associated with healthcare will serve individuals well in the future and help them make better decisions for their overall well-being.

FREQUENTLY ASKED QUESTIONS:

Q: What rights do I have if my insurance company denies coverage for a service?

You have the right to ask your plan to reconsider its decision. If your plan still denies payment after considering your appeal, the law permits you to have an independent review organization decide whether to uphold or overturn the plan’s decision. This final check is often referred to as an external review.

If you’re not satisfied with the way your insurance company addresses your appeal or if you need help, every state has an insurance department you can contact about your coverage. To find out more, contact your state insurance department. Your state may also have a consumer assistance program that can help you file an appeal. Ask your state insurance department if your state has such a program. Finally, contact the National Patient Advocate Foundation on their website or (800) 532-5274, may also be able to help you file an appeal with your insurance company.

Q: If I’m having problems with my insurance, where can I file a complaint?

If you’re not satisfied with your health plan’s services or if your claim has been denied, call the member services phone number on your health plan member card. You may be able to resolve your concern over the phone, or you or your representative can file a complaint with the health plan.

If you decide to file a complaint, you may need to complete a form and submit it in writing so the health plan can investigate the facts, decide what to do, and share any action being taken to address your complaint. You should receive a letter that explains how your complaint was resolved. It will include your appeal rights and how to submit an appeal if you want the health plan to reconsider its decision.

If you’re not satisfied with how your insurance company addresses your complaint, every state has an insurance department to help with questions or complaints. To find out more, contact your state insurance department. Ask if your state has a consumer assistance program that can help you file an appeal. The National Patient Advocate Foundation may be able to help you file an appeal or resolve billing or other complaints with your insurance company. You can also call them at (800) 532-5274.