ACA Coverage Levels Explained | All You Need To Know In 2024

As we approach 2025, the Affordable Care Act (ACA) continues to play a pivotal role in providing accessible healthcare to millions of Americans. Projections indicate that federal subsidies for health insurance are expected to grow substantially, reaching $3.3 trillion, or 8.3% of GDP, by 2033.

This underscores the increasing reliance on ACA provisions to ensure comprehensive coverage. Notably, over 85% of Marketplace enrollees received premium subsidies in 2023, reducing costs by an average of $530 per month. Understanding the ACA’s coverage levels including Bronze, Silver, Gold, and Platinum is essential for selecting a plan that aligns with your healthcare needs and financial situation.

This article provides a comprehensive guide to the ACA coverage levels, helping you make informed decisions about your healthcare plan.

Read More: How To Choose Health Insurance as a Self-Employed | Step-By-Step Guide 2025

Key Takeaways:

- ACA coverage levels are categorized into Bronze, Silver, Gold, and Platinum, offering varying cost-sharing options between premiums and out-of-pocket expenses.

- Bronze plans have the lowest premiums but the highest out-of-pocket costs, ideal for healthy individuals with minimal healthcare needs.

- Silver plans are the most popular due to Cost-Sharing Reductions (CSRs), balancing premiums and out-of-pocket costs.

- Gold and Platinum plans offer higher premiums with lower out-of-pocket costs, suitable for those requiring frequent or extensive medical care.

- Subsidies like premium tax credits and CSRs make ACA plans more affordable, especially for low-income individuals.

Table of Contents

ACA Coverage Levels:

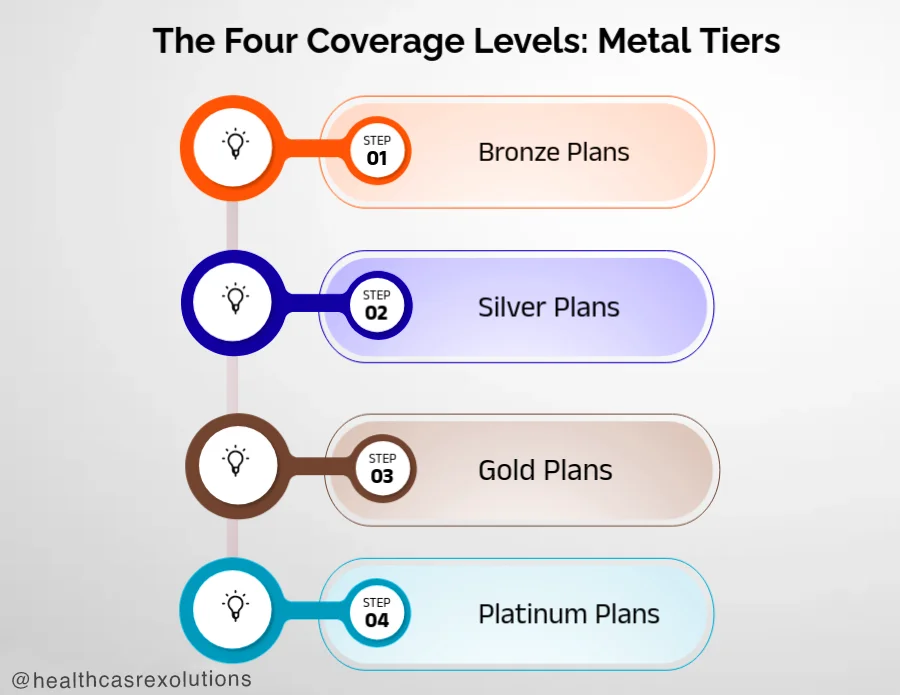

ACA coverage levels, also known as metal tiers, are divided into Bronze, Silver, Gold, and Platinum. These tiers represent the cost-sharing structure between premiums and out-of-pocket expenses but do not reflect the quality of care.

4 Types Of ACA Coverage Levels: Ultimate Guide

Each ACA health plan is categorized into one of four metal tiers: Bronze, Silver, Gold, and Platinum. These tiers reflect the balance between monthly premiums and out-of-pocket costs like deductibles, copayments, and coinsurance. Importantly, the metal tier doesn’t indicate the quality of care—rather, it represents how you and your insurance plan share costs.

1. Bronze Plans:

- Premium: Lowest

- Out-of-Pocket Costs: Highest

- Insurance Covers: About 60% of healthcare costs

- You Pay: About 40% of healthcare costs

Bronze plans are ideal for individuals seeking the lowest monthly premiums and are willing to accept higher out-of-pocket costs when they need care. These plans usually have high deductibles and are suitable for young, healthy individuals who don’t expect to need many medical services throughout the year.

Who is it for? Bronze plans are ideal for people who want to protect themselves against worst-case scenarios, such as serious illnesses or accidents, and who are comfortable paying higher costs when they do need care. However, they may not be the best option if you expect to use healthcare services regularly.

2. Silver Plans:

- Premium: Moderate

- Out-of-Pocket Costs: Moderate

- Insurance Covers: About 70% of healthcare costs

- You Pay: About 30% of healthcare costs

Silver plans strike a balance between affordable monthly premiums and manageable out-of-pocket costs. They’re the most popular option in the Marketplace, partly because individuals and families with low to moderate incomes may qualify for Cost-Sharing Reductions (CSRs). These reductions lower out-of-pocket expenses like deductibles, copayments, and coinsurance, but only if you choose a Silver plan.

Who is it for? Silver plans are suitable for individuals or families looking for a balance between premium costs and out-of-pocket expenses. They’re also ideal for those who qualify for subsidies, as CSRs are only available with Silver plans, making them more affordable than other options.

3. Gold Plans:

- Premium: Higher

- Out-of-Pocket Costs: Lower

- Insurance Covers: About 80% of healthcare costs

- You Pay: About 20% of healthcare costs

Gold plans come with higher monthly premiums but lower out-of-pocket costs when you need care. This means lower deductibles, copayments, and coinsurance. Gold plans are a good choice if you expect to need regular medical care or prescription drugs, as they minimize your out-of-pocket spending.

Who is it for? Gold plans are ideal for individuals who anticipate using healthcare services frequently throughout the year or those who want the peace of mind that comes with lower out-of-pocket expenses. These plans are often best for people with chronic health conditions or those who prefer to pay more upfront in exchange for better coverage when they need care.

4. Platinum Plans:

- Premium: Highest

- Out-of-Pocket Costs: Lowest

- Insurance Covers: About 90% of healthcare costs

- You Pay: About 10% of healthcare costs

Platinum plans have the highest premiums but the lowest out-of-pocket costs. They offer the most comprehensive coverage, making them ideal for individuals who expect to have significant medical expenses throughout the year. These plans generally have very low deductibles and cover a large portion of your healthcare costs, which means you’ll pay very little when you need care.

Who is it for? Platinum plans are best for individuals who anticipate needing a lot of medical care and want to minimize their out-of-pocket expenses. Although the monthly premiums are higher, Platinum plans can save you money in the long run if you require extensive healthcare services, such as frequent doctor visits, surgeries, or ongoing treatments.

The Impact of Subsidies On ACA Levels Of Coverage:

One of the most important features of ACA plans is the availability of subsidies that can significantly lower the cost of premiums.

The two main types of subsidies are:

- Premium Tax Credits: These help lower the cost of monthly premiums and are available to individuals and families with incomes between 100% and 400% of the federal poverty level (FPL). Under recent changes from the American Rescue Plan and Inflation Reduction Act, some individuals with incomes above 400% of the FPL may still qualify for tax credits.

- Cost-Sharing Reductions (CSRs): As mentioned earlier, CSRs lower your out-of-pocket costs but are only available with Silver plans. These reductions make Silver plans particularly appealing to individuals with lower incomes.

How To Choose The Right Affordable Care Act Plan?

When selecting an ACA plan, it’s crucial to consider your health status, budget, and expected healthcare needs. Here are some key factors to think about:

- Monthly Premium vs. Out-of-Pocket Costs: Do you prefer lower monthly payments with higher costs when you need care (Bronze), or are you willing to pay higher premiums for more coverage and lower out-of-pocket costs (Gold or Platinum)?

- Your Health Needs: If you’re generally healthy and rarely need medical care, a Bronze or Silver plan might be suitable. However, if you have a chronic condition or expect to need frequent medical services, a Gold or Platinum plan might save you money in the long run.

- Subsidy Eligibility: If you qualify for premium tax credits or cost-sharing reductions, a Silver plan may offer the best value, as it provides a good balance between premiums and out-of-pocket costs with the potential for reduced costs through subsidies.

- Risk Tolerance: Consider how comfortable you are with taking on the risk of higher out-of-pocket costs if something unexpected happens, such as a serious illness or accident. Lower-tier plans come with this risk, while higher-tier plans provide more financial protection.

Conclusion – ACA Coverage Levels:

Choosing the right ACA tier of coverage involves a careful evaluation of your health needs, financial situation, and risk tolerance. The Bronze, Silver, Gold, and Platinum tiers offer different ACA coverage levels, each with a unique balance between monthly premiums and out-of-pocket costs. Whether you need basic coverage or comprehensive protection, understanding these tiers and any available subsidies can help you make an informed decision.

FAQ’s:

What are the four tiers of ACA?

ACA tiers are Bronze, Silver, Gold, and Platinum. They represent the cost-sharing ratio of premiums and out-of-pocket expenses, offering varying coverage options.

What is the coverage level?

Coverage levels indicate the percentage of healthcare costs paid by insurance versus the individual. Bronze covers 60%, Silver 70%, Gold 80%, and Platinum 90%.